Four Proven Ways to Build Home Equity Quickly

Owning more and owing less is the heart of home equity, and here are proven ways to tilt the seesaw in your favor faster.

Whether you're looking into a possible cash-out refinance, a home equity line of credit (HELOC), or selling your home for a tidy profit, at the center of every consideration will be your home equity. Chances are it's the most valuable thing you own.

For many people, the home they bought is not only a place to live and put down roots but also their biggest asset. The most recent study by the Pew Research Center found that 81% of Americans agree that buying a home is the best long-term investment a person can make¹ and they put their money where their mouth is. They buy homes. In every study, home ownership eclipses all other assets, such as investment accounts and savings.

Buying a home is of course where mortgages come into play. You could think of a mortgage as a forced savings plan. Every payment you make deposits more money in the home. So long as the home's value keeps climbing, so does your savings.

The home is many people's single biggest retirement plan too, either as a place to live mortgage-free after the home loan is paid off, or as a source of income after selling and downsizing.

Equity (noun) eq·ui·ty: The difference between your home's market value and what you owe.

Think of "value" and "owe" as two dials: turn the Value dial up or the Owe dial down—or better yet, turn both—and you increase home equity.

What's great about home ownership as an investment is that the Value dial tends to turn up on its own thanks to appreciation, and as you make the monthly mortgage payments the Owe dial turns down too. Home equity definitely grows in your home, but is it growing fast enough for you?

What can you do to crank one dial or the other, or both? Let's discuss four tried-and-true ways that people can build home equity faster.

Make a Bigger Down Payment for Instant Home Equity

Making a large down payment establishes your equity in the home immediately. Instantly you own more and owe less. If you can swing a down payment of 20%, you build equity even faster because more of your monthly payment can go toward the home itself (the loan principal) and not toward private mortgage insurance (PMI).

Lenders require PMI on mortgages with down payments under 20%. This insurance covers the lender but is paid for by the homeowner. That's money that could go toward the principal instead and thus build home equity faster.

A National Association of Realtors (NAR) study found that the median down payment for all homebuyers in 2022 was 13%, with younger people putting down the least. The median down payment climbed as homebuyers grew older:

- All buyers: 13%

- Age 22-31: 8%

- Age 32-41: 10%

- Age 42-56: 15%

- Age 57-66: 21%

- Age 67-75: 28%

- Age 76-96: 30%

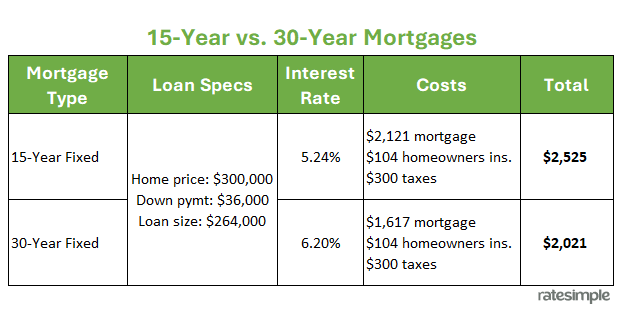

A 15-Year Mortgage Builds Home Equity Much Faster

The 30-year fixed-rate mortgage is the most popular, but cutting the term to 15 years would yield big savings in interest while accumulating equity much faster. Your monthly payment under a 15-year mortgage would be higher for sure, but contrary to what you might expect, it wouldn't be double the payment you'd make on a 30-year mortgage. Your payment would be around one-quarter higher with a 15-year term compared to a 30, as you can see from the table below.

A 15-year mortgage gets you to the finish line—100% equity—in half the time, and you saved huge money on interest.

Comparison of 15- and 30-year mortgages.

If you finance a home for $264,000 at 5.24% interest over 15 years, you’ll pay $117,753 in total interest. However, if you finance that same home at 6.20% for 30 years (30-year fixed rates are always higher), you’ll pay a whopping $318,091 in pure interest. (At the time of writing, those rates were the national averages.)

The savings is so substantial with a 15-year mortgage that homebuyers would do well to consider buying a less expensive home if it means they would be able to manage higher payments and reach full home equity in just 15 years.

Plus, it's not a lot more expensive to go with 15 years; it's about 25% more given the current interest rates, as you can see in this table. And you would reach 20% equity much faster, which is when PMI stops—another savings.

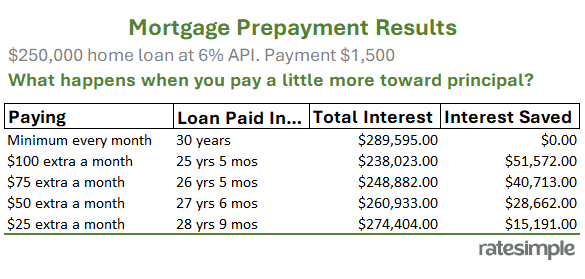

Pay a Little More Towards the Principal Each Month

Adding a Benjamin to your payment each month can improve your household finances (see table below). After only five years, that extra $100 will have built up more than $7,000 in extra equity. See the table below for the surprising amount of money a few extra dollars saves you on interest and the years that it shaves off the loan.

Rather than $100 a month, another approach is to make an extra payment every year, or the equivalent. You could use an annual bonus or other windfall, but another strategy is to pay one-twelfth extra each month. So if your official payment is $1,500, divide this by 12 to get $125 and that's how much extra to pay each month. At the end of each year, you will have made the equivalent of 13 payments.

Another way to make 13 payments a year takes less effort. Just pay your mortgage biweekly if your lender allows it. Paying half the monthly payment every two weeks is the equivalent of 13 monthly payments, because there are 26 half-months in the year.

Paying down the principal sooner dramatically cuts the amount of interest you pay over the life of the loan.

Whichever method you use to pay a little extra each month, ask your lender how you can ensure that the extra goes 100% toward the loan principal, not the interest. Examine your monthly statements to make sure it happens. Only the money you pay toward the principal—not the interest—actually builds equity.

Home Improvements to Boost Home Equity

Remember that home equity is the difference between the home's market value and how much you owe on it. So far we have talked about turning down the Owe dial quicker, but what about turning up the Value dial?

You have little control over home values in your neighborhood or town, much less the local and national economies, but you do control your home improvements. Consider these minor home improvement projects to add value to your home and thus build equity without the expense or hassle of major renovations.

- Improve curb appeal. An investment in fresh paint, fixing broken roof tiles, landscaping, and upgrading other features of your home's exterior typically brings a 100% return.

- Minor bathroom upgrade. Recaulk and glaze the bathtub, replace the toilet, repaint the walls, or swap out carpet for hard flooring. Little improvements in the john can raise home value a lot.

- Kitchen facelift. Stick to minor improvements like refaced cabinets and new appliances to see the biggest return on investment. The sledgehammer renovations that make for such good TV are an ordeal for homeowners.

- Add living space outdoors. Tricking out a patio with a firepit and more seating is a cost-effective means of adding living space. Same with building a wooden deck. It is estimated that you can expect a 75% return on investment when you build a deck.

Get an Idea How Much Your Home Is Worth

To estimate how much your home is worth today, you can use this calculator at the Federal Finance Housing Agency. You enter your state, the purchase price, and the start/end dates to see how much the value of your home has changed since you bought it.

Estimates by Zillow can also give you a ballpark idea of your home's worth, although you should take those "Zestimates" with a grain of salt, cautioned realtor Bill Gassett. "Zillow and their Zestimate of value is not accurate," he stated bluntly in an advice forum. "In fact, if you look at the fine print on their site they will tell you so themselves. Their accuracy is appalling."

Gassett pointed out that the online service just doesn't know enough about your home to evaluate it. "Does anyone from Zillow visit your home to check on accuracy or information? No, they do not! Does Zillow know you just dumped $75,000 in improvements into your home? No!"

Key Takeaways

- Equity is your home's value minus what you owe on it.

- Ways to quickly lower what you owe include a larger down payment, paying a bit extra each month, and opting for a 15-year term.

- Smart home improvements can raise value as quickly as you can complete the project.